June 10, 2013

In May 2004 General Electric (GE) spun off many of its financial operations into a new company called Genworth (GNW). These operations included domestic and international mortgage insurance, life and long-term care insurance, international payment protection insurance, and wealth management. The financial crisis of 2008 nearly swamped the new company, due to huge losses in its U.S. mortgage insurance business. Genworth has been digging out ever since: shedding non-core product lines, bringing in new management, and improving its capital structure.

One product line that the company has retained is long-term care (LTC) insurance. The question is, can GNW really make enough money in this product to make it worth keeping?

At first glance, long-term care insurance would appear to be a very attractive product to an aging demographic. GNW’s website states that at least 70% of people over 65 will need long term care services at some time in their lives. Nationally, the median cost for a private nursing home is over $80,000 per year. Long-term care provides payments to policyholders who need help with daily activities such as bathing, dressing, eating, and toileting.

GNW (and formerly GE) has been a leader in LTC for over 35 years. Policies are priced using actuarial data and projections for mortality, morbidity, health care costs, lapse rates and interest rates. The huge problem for GNW is that these historical assumptions have been incorrect. People have been living longer, while health care costs have escalated. Policyholders have held onto their policies, making lapse rates much lower than expected. And low interest rates have made it very challenging to generate strong investment returns to help support the product. GNW’s annual loss ratios in LTC have ranged from 65% to 71% over last five years, increasing over the past several years.

These problems are not unique to GNW. Many competitors, also struggling with underpriced books of business, have exited the market. Those who still offer the product have significantly raised pricing or reduced policy benefits. These changes have caused industry annualized first-year premiums of individual long-term care policies to drop from their peak of $1 billion in 2002, down to $608 million in 2006 and about $580 million in 2012. (Data from LIMRA International and GNW’s 2012 10K)

Like its competitors, GNW has been raising prices and redesigning its products to improve profitability. In November 2010 the company filed for premium rate increases of 18% on two blocks of older long-term care policies. In the third quarter of 2012, GNW initiated another round of long-term care premium increases, raising rates 50% on older generation policies and 25% on new generation policies. These changes are expected to increase annual premiums by $200-300 million.

However, rate approvals are granted on a state-by-state basis, which is a very slow process. As of December 31, 2012, GNW had received approvals for 86% of targeted premiums in the 2010 price increase, and 20% of premiums in the 2012 price increase. The company estimates it will take five years to implement all projected price increases.

To improve profitability, GNW has also temporarily suspended LTC sales in California. It also ended a five-year sales initiative with AARP, initiated in 2007.

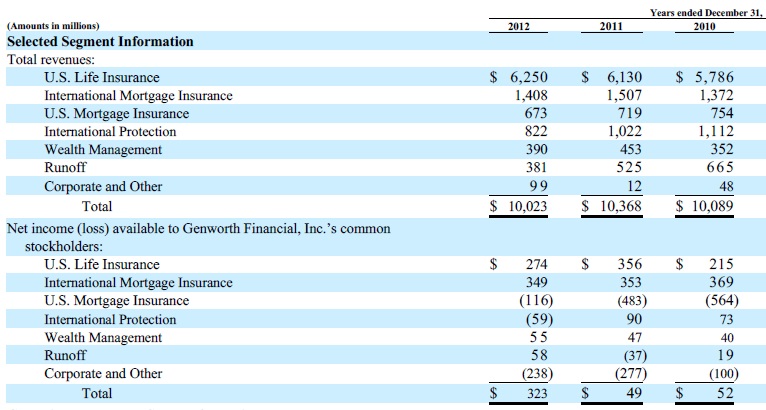

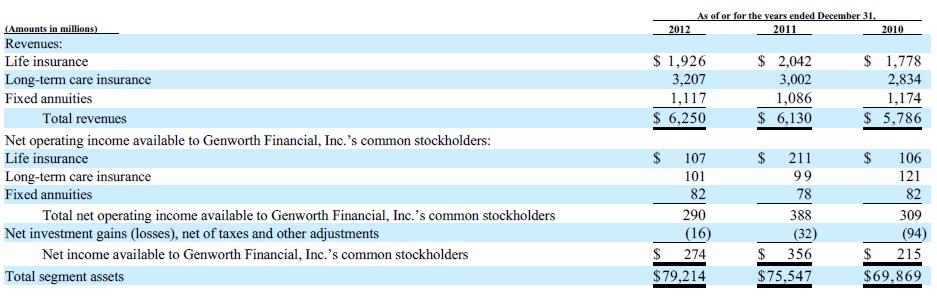

Will all these changes make LTC a more profitable product for GNW? LTC insurance is reported under the U.S. Life Insurance segment. As indicated in the following two charts from GNW’s 2012 10K, LTC contributed 28-32% of total company revenues in the past three years. It accounted for 31% of net income in 2012. Unfortunately, the net operating margin on this product was only 4.3% in 2010, 3.3% in 2011, and 3.2% in 2012.

Quarterly results show slow progress, as seen in the charts below from the 1Q2013 company presentation. Premiums and net investment income and yield have been in a small range over the past five quarters, but the company is still struggling with the net operating margin on its LTC product. The 1Q2013 margin was 2.6%, down from 4.5% in 1Q2012.

In summary, GNW has taken significant steps to improve the profitability of its underpriced LTC product. However, because rate increases are approved on a state-by-state basis, the company projects it will take five years to achieve the projected premium increases on its LTC book of business.

GNW has shed a number of non-core business over the past few years, including variable annuities, variable life insurance, institutional, corporate-owned life insurance, and Medicare supplement insurance products. Both International Protection and Wealth Management were added to the non-core list, and the Wealth Management business was recently sold for $412.5 million. Long-term care insurance is only marginally profitable. If operating margins in this product do not make steady improvements, it is possible that LTC could be added to that non-core list.

Disclosure: I own some GNW stock.

Very interesting, eye-opening look into the LTC business. If GNW were to shed the LTC, what would it have left at its “core”?

The primary businesses would be domestic and international mortgage insurance, as well as life insurance.