June 15, 2013

Most financial advisors have typically recommended that investors allocate a certain percentage of their portfolio to bonds. Depending on your age, risk tolerance, and income needs, that percentage may range from 25-40% or even higher. Historically, bonds have not only supplied steady income to a portfolio, but have also reduced overall risk levels.

Those recommendations are now changing. Many advisors are suggesting limiting exposure to bonds, especially longer term ones, and some are advocating getting out of bonds altogether. Why the change in opinion?

It’s all about interest rates.

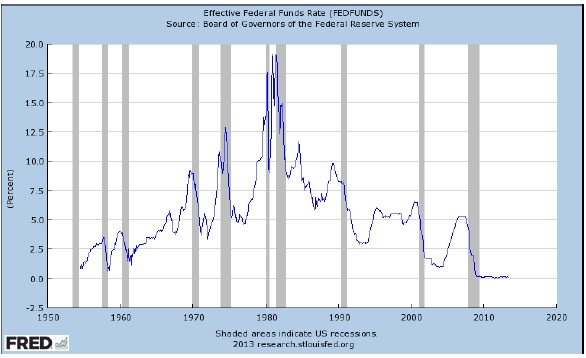

Bond prices have an inverse relationships to interest rates. That means as interest rates go down, bond prices go up. As you can see from the following chart, interest rates have been going down for over 30 years, ever since their peak in the 1980’s. This has created a golden age in bond investing.

But now interest rates appear to be about as low as they possibly can get. In fact, rates have been approaching zero. Why? Because when interest rates spiked up during the 2008 financial crisis, the Federal Reserve began its quantitative easing program. This meant the Fed bought up lots of Treasury bonds and mortgage-backed securities (MBS). Their purchases drove prices up, and interest rates down.

The market now feels the Fed is likely to taper off its bond purchases. This will decrease demand for bonds, pushing bond prices lower and interest rates higher.

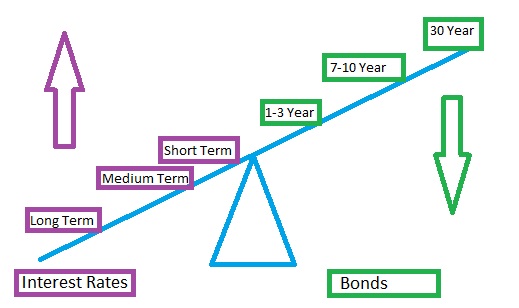

Longer term bonds are more sensitive to interest rate changes.

Longer term bonds are more sensitive to interest rate changes than shorter term ones. This sensitivity is called duration. The concept can be illustrated in the seesaw below. Long term bonds sit at one end of the seesaw. Long term interest rates sit at the other end. As the seesaw moves, the ends move much more than the center.

This means that as interest rates go up, long term bond prices will go down the most. Medium and shorter term bonds, which are nearer the fulcrum of the seesaw, will go down less.

How do these changes impact your investments?

The chart below compares returns for three Vanguard bond exchange traded funds as of 5/30/2013, a long term bond fund BLV, an intermediate term bond fund BND, and a short term bond fund BSV. (These funds were chosen for illustrative purposes only. There are many bond funds and exchange traded funds available. I am not making a recommendation regarding any of them).

What does this chart tell you?

- That year to date, if you are invested in these funds, you are losing money.

- The longer term your bond fund, the more money you are losing. The long term BLV is down 3.7% year to date, while the intermediate term BND is down 1.01% and the short term BSV is down 0.02%.

So what should you do to generate income in your portfolio?

- If you want to invest in a bond fund, focus on short-to-intermediate duration funds. The shorter term bond funds will pay out a lower interest rate, but they will go down less as interest rates rise.

- Trim your exposure to long term bonds, but do not sell all your holdings. Bond prices have already moved down in consensus anticipation of higher interest rates. If the Fed goes against consensus and announces it does not plan to taper its bond purchases, then rates will soften and bond prices will go up. Delay new purchases of long term bonds until there is more clarity on the future direction of rates.

- Consider investing in individual bonds which you can hold until maturity, rather than in bond funds or ETFs. Consult your financial advisor to structure a bond ladder composed of various bonds of different maturities. Note that you will probably need to invest at least $200,000 to achieve a diversified bond portfolio.

- Seek income from other sources, such as dividend-paying stocks, preferred stocks and real estate investment trusts (REITs). The prices of these investments also have interest rate sensitivity, which I will discuss in future articles.

When is the best time to buy bonds?

Remember that the best time to buy bonds is when interest rates are high but headed lower. In that situation, buy longer term bonds, which will go up more as interest rates go down.

The worst time to buy bonds is when interest rates are low and headed higher, which appears to be where we are now. All bond prices will go down, but longer term bonds will go down the most. If you want to buy bonds in a rising interest rate environment, buy shorter term ones.