July 10, 2013

Until its price peak in late 2011, gold had been in a twelve year bull market. Its price appreciation accelerated following the 2008 financial crisis, more than doubling from less than $800 an ounce in 2008 to over $1,800 per ounce in 2011. During 2013, however, gold lost its glitter. The price fell 3.6% during the first quarter, and another 10% during two days in April. As of July 9, the price was $1,247.80, down about 30% from its 2011 peak.

What drove the price fluctuations?

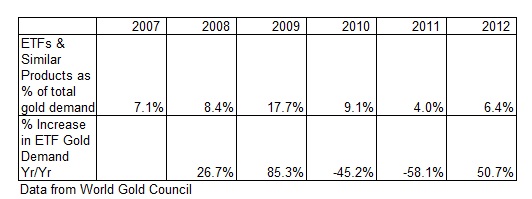

Following the 2008 financial crisis, investors rushed into gold as a safe haven in an uncertain world, primarily through gold-backed exchange traded funds (ETFs), which were first introduced in 2003. According to the World Gold Council, although total gold demand in 2009 decreased 11% to 3,385.8 tons as rising prices depressed jewelry and industrial demand, investment demand showed strong gains. ETF demand increased 85% to 594.7 tons, representing 17.6% of total gold demand. ETFs had represented only 7.1% of gold demand in 2007 and 8.4% of in 2008.

Much of the ETF money went into the SPDR Gold Shares Trust (GLD), the largest of the gold-backed ETFs, with assets of $37 billion. A smaller gold-backed ETF is the iShares Gold Trust (IAU), with assets of almost $7 billion. Another popular way to play the increase in gold was through investment in the Market Vectors Gold Miners ETF (GDX), whose top holdings are Goldcorp (GG), Barrick Gold (ABX), and Newmont Mining (NEM). These investments did very well in 2009 and 2010, as shown in the chart below.

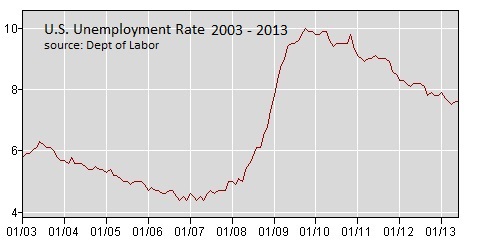

The enthusiasm for gold started to fade in late 2011. Economic conditions were improving. Unemployment rates were coming down. And investors rushed to the exits, locking in their profits. ETF demand as a percentage of total gold demand fell sharply.

Volatility continued in 2012. Gold demand dropped 4% to 4,405.5 tons as overall investment demand, which includes physical bars and coins as well as ETFs, continued to decline, outweighing increased purchases by central banks and increased jewelry demand, primarily from India and China. Investment demand was 35% of total gold demand, compared to 44% from jewelry, 9% from technology/industry, and 12% from Central Bank purchases.

The price drop in 2013 accelerated, especially after Cyprus sold reserves to cover losses from emergency loans to its banks. The U.S. economy, in contrast, continued to improve, causing investors to continue to desert their safe haven asset.

Is Gold a Good Value Now?

Now that gold is down about 25% in 2013, is it a good value? Should you put this asset back in your portfolio?

The truth is, it is very difficult to determine the appropriate price for gold. It does not pay a dividend. It does generate any cash flow. It has no book value. Therefore, many of the metrics we routinely use to evaluate stocks just do not work for evaluating gold. We do know that the valuation is down to 2010 levels, but it is difficult to determine if there is further downside.

Why Put Gold in a Portfolio?

Why do investors like to have gold in their portfolios?

- To hedge against inflation,

- To hedge against a declining dollar,

- To provide a safe haven during geopolitical and financial instability, and

- To diversify their portfolios and reduce risk.

Looking at each of these measures, it is difficult to make a compelling case for gold.

- Inflation is not yet a threat. According to the U.S. Bureau of Labor Statistics, the Consumer Price Index increased 0.1% in May on a seasonally adjusted basis. Over the last 12 months, the index was up 1.4% before seasonal adjustment.

- After almost 10 years of weakening against major currencies, the U.S. dollar appears to be strengthening, as shown in the chart below from the St. Louis Fed.

- While many international economies are still struggling, the U.S. economy appears to be on firmer footing. The unemployment rate is going down. In June it dropped to 7.6%, near the Federal Reserve’s 7% target for ending its $85 billion per month bond buying program and its 6.5% target for potentially raising interest rates.

- A well diversified portfolio is very important, and gold can reduce risk under the appropriate conditions. However, the stock market is getting stronger. The SPX is up 15.86% YTD. And bond prices are getting more attractive as interest rates rise. Under these conditions, it is difficult to make a table-pounding case for gold.

Don’t Rush to Get Back Into Gold

Many financial advisors advocate a 5% weighting in gold, for the reasons already discussed: as an inflation hedge, a dollar hedge, a political/economic safe haven, and a portfolio diversifier. Although these issues do not appear to be threats at the moment, situations in the market can change quickly. A small allocation to gold is probably prudent, but there is no sense of urgency to buy gold now.

The prices of the two major gold ETFs, GLD and IAU, are both down 25% year to date. While they have rallied back up about 2% from their June lows, it is too early to call a bottom. Wait for further evidence of price stability before adding this asset to your portfolio.

Disclosure: I own IAU.