February 18, 2015

- Genworth reported a 4Q14 operating loss of $416 million, or $0.84 per diluted share, below analysts’ consensus estimates of a loss of $0.13.

- While the mortgage insurance (MI) business segments performed well, long term care (LTC) continued to negatively impact the company. Quarterly results included a $478 million charge for long term care and a $274 million write off of goodwill.

- External advisors have been hired to undertake a financial and strategic review of the company. Management plans to reduce debt by $1 to 2 billion to increase financial flexibility. CEO McInerney admitted that a number of investors have discussed splitting the mortgage insurance and life insurance operations.

Genworth reported a 4Q14 operating loss of $416 million, or $0.84 per diluted share, below analysts’ consensus estimates of a loss of $0.13. This compares to a net operating loss of $0.64 per share in 3Q14, and a net operating profit of $0.38 per share in 4Q13.

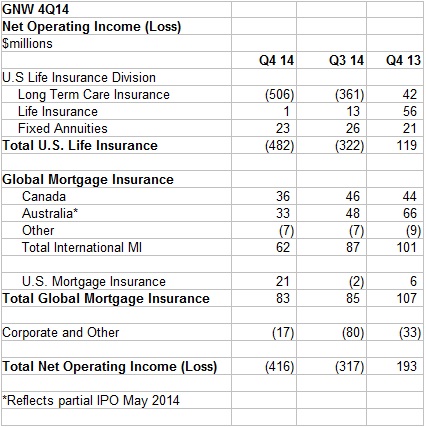

While the global mortgage insurance was profitable, LTC continues to struggle. Segment results are shown in the chart below. (Source: Company reports)

Long term care insurance (LTC) continues to be the biggest drag on results.

The company conducted a major review of the business line in the quarter, resulting in the $478 million charge. Revised assumptions expect policies to be in claim status for longer periods and to use higher levels of benefits. Going forward, GNW will implement a rolling 12 month average to “self adjust” utilization rates as policies age.

Hopefully, the $345 million charge in 3Q14 and $478 million charge in 4Q14 means that there are no more large charges to come in this business line. Profitability, however, is still elusive. GNW needs state-approved price increases and/or benefit reductions to bring the older blocks of business to break-even status and to improve profitability on the newer blocks. The 2012 rate action (covers Pre-PCS, PCS I, PCS II and Choice I lines) is expected to add $250 to $300 million to annual premiums. Price increases on Choice II premiums are expected to add another $40-60 million. As of YE 2014, 22 states had approved the Choice II premium increases and 8 had initially disapproved them. GNW will go back to the states that did not grant approvals to request that they reconsider the price increases.

GNW has redesigned its LTC products to achieve higher returns, with lower risk for the company. They plan to impress on regulators the need to consider more frequent and smaller premium increases on current and future business. It appears that LTC has become a “bait and switch” product. The company sells the product with a given premium, knowing that it will either increase the premium and/or reduce the benefits in future years if it becomes unprofitable. The implication is that if the product were appropriately priced at policy inception, it would be cost-prohibitive to the buyer.

Sales have suffered as consumers have become more aware of this strategy. Individual LTC sales were $17 million in 4Q14, down 39% from 3Q14 and down 29% from 4Q13, as shown in the chart below (source: company reports).

The Global Mortgage Insurance (MI) segment remains profitable.

The Canadian and Australian operations are profitable and continue to upstream dividends to the holding company. Results in 2014 were good, but the company admitted that losses were unsustainably low. The full year loss ratio for Canada was 20%, and is projected at 20-30% for 2015. The full year loss ratio for Australia was 19%, and is projected at 25-30% for 2015. Falling commodity prices will negatively impact both of those countries.

The U.S. MI segment continued to strengthen. It had a 19% drop in new flow delinquencies compared to last year. The loss ratio in 2014 was 62%, and is projected to drop to 40-50% for 2015. This segment has shown steady improvement but is not expected to generate significant cash dividends to the holding company for several years. Additionally, it will need $500 to 700 million in additional capital to meet new GSE eligibility requirements.

External advisors have been hired to undertake a financial and strategic review of the company.

Management says it has no plans to raise capital at this time, since it has excess liquidity at the holding company level and solid capital levels. Alternative sources of funds are a $100 million cost reduction program, the sale of the noncore lifestyle protection insurance business (albeit at a significant loss on sale), additional life block sales, and the refinancing or reinsurance of mortgage insurance (MI) risks. Another source is the sale of more of its Australian MI business (a partial IPO was completed in May 2014).

GNW plans to reduce debt by $1 to 2 billion. The current debt to capital ratio is 25.9%, which is in line with similar companies. During the earnings call, CEO McInerney was questioned about why GNW felt it needed to reduce debt. He admitted that a number of investors had been talking with the company about splitting the profitable mortgage insurance operations away from the challenged life insurance/LTC operations. The debt reduction will give the company more flexibility in considering various options.

Valuation and Stock Performance

The stock immediately rallied almost 7% following the earning report, but is still down 53% from its May 2014 peak. The price/tangible book value, excluding accumulated other comprehensive income, is around 0.42. Operating return on equity was a negative 15.3% for 4Q14, and a negative 3.3% for the full year. Current results justify the low valuation.

What about going forward? Does the future look brighter from here? Mortgage insurance is performing well, but the Australian and Canadian operations face higher default risk going forward from lower commodity prices. In addition, management has said it might sell off more of the Australian operations in order to generate more cash flow. The real key to a turnaround is improvement in LTC profitability, which will be a long, slow process.

The hiring of external advisors and the planned $1-2 billion in debt reduction imply that GNW is considering either selling or splitting the company. Patient investors could see a higher return if the company followed that strategy, although it is not likely to happen in the near term.